Global Polyalphaolefin (PAO) Market Report (2025-2036):

Global Polyalphaolefin (PAO) Market Size and Growth Forecast

Global Polyalphaolefin (PAO) Market is projected to grow from USD 2625 million in 2025 to USD 4691 million by 2036, registering a CAGR of 5.43% during the forecast period. Recognized as an API Group IV synthetic base stock, Polyalphaolefin is meticulously manufactured through the catalytic oligomerization and subsequent hydrogenation of linear alpha-olefin monomers, predominantly utilizing 1-decene, 1-dodecene, or 1-octene to yield a highly uniform hydrocarbon molecular architecture. This advanced synthesis works by mirroring the core lubricating application of conventional mineral base oils but replacing naturally occurring, irregular crude oil fractions with precisely engineered, pure synthetic saturated olefin oligomers. This tailored chemical structure grants PAO profound competitive advantages over traditional mineral alternatives, particularly by delivering exceptional shear stability, superior thermal resistance characterized by a highly elevated viscosity index, and outstanding low-temperature pour points that prevent crystallization in extreme sub-zero environments. Furthermore, the complete absence of inherent impurities such as sulfur, nitrogen, aromatics, and reactive ring structures imparts excellent oxidative stability, remarkably low volatility, and enhanced lubricity, significantly mitigating friction and mechanical wear in high-stress processing operations. The robust structural expansion of this chemical sector is heavily underpinned by the global transition toward high-performance automotive and industrial lubricants, propelled by increasingly stringent environmental regulations that mandate maximized fuel efficiency, lower emissions, and extended drain intervals. Concurrently, rapid industrialization, expanding commercial transportation networks, and massive capital investments in renewable energy infrastructure—most notably the widespread deployment of wind turbine gearboxes requiring highly durable, extended-life synthetic lubrication—throughout the Asia-Pacific and European regions are acting as primary macroeconomic catalysts, firmly sustaining the accelerated regional demand for these premium synthetic base fluids.

Polyalphaolefin (PAO) Applications in Packaging and Construction Industries

Polyalphaolefin (PAO) is predominantly utilized within the automotive and industrial lubricant sectors, where it serves as a critical synthetic base oil for advanced engine oils, gear lubricants, compressor fluids, and heavy-duty greases. This material is specifically chosen for these high-stress applications due to its exceptional physical properties, including a highly uniform, wax-free molecular structure that delivers an outstanding viscosity index, superior thermal and oxidative stability, and an exceptionally low pour point, all of which ensure optimal lubrication and equipment protection across extreme temperature variations. The demand for PAO is powerfully propelled by the technical superiority it offers over conventional mineral oils, particularly in maximizing mechanical efficiency, preventing shear loss, and reducing internal friction in modern, high-performance engines and industrial machinery. Furthermore, consumer and industrial focus on operational efficiency acts as a major catalyst for adoption, as PAO-based formulations significantly extend oil drain intervals and improve fuel economy, thereby decreasing maintenance downtime and reducing waste generation to align with broader industrial sustainability targets for energy conservation. Consequently, the overall market trajectory for this synthetic polymer points toward robust expansion, characterized by increasing market penetration in emerging industrial sectors and a growing demand for advanced, energy-efficient lubrication solutions that support next-generation hardware development.

Global Polyalphaolefin (PAO) Market Segmentation by Resin Type and End-Use Application

The global polyalphaolefin (PAO) market is primarily segmented by application into engine oils, gear oils, compressor oils, hydraulic fluids, and greases, as well as by end-user industry across the automotive, industrial machinery, aerospace, and marine sectors. Within these classifications, the automotive engine oil segment currently maintains the leading position, commanding a dominant share of the overall market. This sustained supremacy is fundamentally attributed to the widespread global adoption of high-performance synthetic lubricants in modern passenger and commercial vehicles, where PAO’s exceptional oxidative stability, inherently high viscosity index, and superior low-temperature flow properties are critically relied upon to extend drain intervals, enhance fleet fuel economy, and ensure compliance with increasingly stringent environmental emission mandates. Conversely, advanced thermal management fluids and specialized industrial gear oils represent the fastest-growing segment with the highest future economic potential. This rapid expansion is heavily propelled by the global transition toward electric mobility and renewable energy generation, creating a surging demand for specialized dielectric cooling fluids utilized in electric vehicle (EV) battery systems, automotive sensors, and heavy-duty gear lubricants required for wind turbine drivetrains. The inherent shear stability, high dielectric strength, and unparalleled thermal conductivity of polyalphaolefins make them technically indispensable for enduring the extreme mechanical loads, rapid heat fluctuations, and high-voltage environments characteristic of these next-generation technologies.

Europe's Dominant Role in the Global Polyalphaolefin (PAO) Market

Europe currently holds the preeminent position in the global polyalphaolefin landscape, dictating overarching market dynamics through a highly evolved industrial and legislative framework. This geographical dominance is fundamentally driven by stringent regulatory policies, most notably rigorous REACH compliance mandates and severe automotive emission frameworks that collectively compel the transition from conventional mineral oils to advanced, low-volatility synthetic base stocks engineered to ensure superior fuel economy and drastically reduced carbon footprints. Complementing these aggressive legislative pressures is a robust regional market sentiment heavily favoring sustainable, energy-efficient operations, which is further fueled by high disposable incomes and an accelerating consumer demand for environmentally responsible, long-lasting industrial and automotive products. Furthermore, the region's undisputed leadership is solidified by massive, sustained financial commitments to advanced tribology research and development, allowing for continuous breakthroughs in catalytic production efficiency and targeted molecular engineering. Propelled by this deeply entrenched culture of regional innovation, Europe is actively spearheading the versatility of polyalphaolefins, deliberately expanding their utilization far beyond standard internal combustion engine lubricants to pioneer complex formulations for cutting-edge sectors, including advanced dielectric thermal management fluids for the rapidly expanding electric mobility infrastructure and high-durability gear oils strictly engineered for offshore wind energy generation.

Recent Developments and Strategic Initiatives (2025)

The global Polyalphaolefin (PAO) market has witnessed targeted capacity additions from late 2024 through early 2026 as manufacturers scale up production to meet growing demand for high-performance synthetic lubricants in automotive, industrial, and emerging electric vehicle applications. Chevron Phillips Chemical Company successfully completed the expansion of its low-viscosity polyalphaolefin production unit at its Beringen site in Belgium, doubling the facility's capacity to 120,000 metric tons per year. Concurrently, INEOS Oligomers advanced a phased expansion of its high-viscosity PAO unit in La Porte, Texas, which is scheduled to become fully effective by mid-2025 and will increase the site's production capability to nearly 40,000 tonnes per annum. These strategic investments reflect the industry's continued capital expenditure to enhance existing product portfolios, particularly as original equipment manufacturers specify more rigorous performance standards requiring excellent thermal stability, low volatility, and improved energy efficiency.

Key Players in the Global Polyalphaolefin (PAO) Market

Major players in the Global Polyalphaolefin (PAO) market are Chevron Phillips Chemical, ExxonMobil Chemical, Ineos Oligomers, Shanxi Lu’An Taihang Lubricants Co Ltd, Others (Shanghai Fox Chem., etc.)

Years considered for this report:

Historical Period: 2015-2024

Base Year: 2025

Estimated Year: 2026

Forecast Period: 2026-2036

This report will be delivered through an online digital platform with a one-year subscription, along with quarterly updates.

Objective of the Study:

• To assess the demand-supply scenario of the Polyalphaolefin (PAO), covering production, demand, and supply at the global level.

• To analyze and forecast the market size of Polyalphaolefin (PAO)

• To classify and forecast the Global Polyalphaolefin (PAO) market based on end-use industries and regional distribution.

• To examine competitive developments in the global Polyalphaolefin (PAO) market, such as expansions, mergers & acquisitions, and other strategic initiatives.

Research Methodology: How Was the Polyalphaolefin (PAO) Market Data Collected?

To extract data for the Global Polyalphaolefin (PAO) market, primary research surveys were conducted with Polyalphaolefin (PAO) manufacturers, suppliers, distributors, wholesalers, and traders. During the interviews, respondents were also asked about their competitors.Through this approach, ChemAnalyst was able to identify and include manufacturers that could not be captured through secondary research due to its limitations.Moreover, ChemAnalyst analyzed various market segments and projected a positive outlook for the Global Polyalphaolefin (PAO) market over the coming years.

ChemAnalyst calculated the global demand for Polyalphaolefin (PAO) by analyzing the volume consumed by end-user industries. The forecast was developed based on the growth rates of these end-use industries. These values were obtained from industry experts and company representatives and were externally validated by analyzing the historical sales data of respective manufacturers to determine the overall market size. Additionally, various secondary sources, such as company websites, association reports, and annual reports, were reviewed by ChemAnalyst.

Key Target Audience for This Report

• Polyalphaolefin (PAO) manufacturers and other industry stakeholders

• Organizations, forums, and alliances related to Polyalphaolefin (PAO) distribution

• Government bodies, including regulatory authorities and policymakers

• Market research organizations and consulting firms

The study provides insights into several critical ques tions relevant to industry stakeholders, including Polyalphaolefin (PAO) manufacturers, customers, and policymakers. It also helps identify high-growth segments over the coming years, thereby supporting stakeholders in making informed investment decisions and facilitating strategic expansion.

Report Scope and Market Segmentation Framework

In this report, the Global Polyalphaolefin (PAO) market has been segmented into the following categories. In addition, key industry trends have been detailed below:

Attribute

Details

Market size Value in 2025

USD 2625 Million

Market size Value in 2036

USD 4691 Million

Growth Rate

CAGR of 5.43% from 2026 to 2036

Base year

2025

Estimated year

2026

Historical Data

2015 - 2024

Forecast period

2027 - 2036

Quantitative units

Demand in thousand tonnes and CAGR from 2026 to 2036

Report coverage

Industry Market Size, Capacity by Company, Capacity by Location, Operating Efficiency, Production by Company, Demand by End- Use, Demand by Region, Demand by Sales Channel, Demand-Supply Gap, Company Share, Manufacturing Process.

Segments covered

By End-Use: (:AutomotiveIndustrial, Electrical Aerospace, Others (Cosmetic etc.). By Sales Channel: (Direct Sale and Indirect Sale)

Regional scope

North America, Europe, Asia Pacific, Middle East and Africa, and South America.

Market Data & Insights

Table of Content

1. Industry Market Size

It is an essential metric for market analysis, as it provides insights into the overall size and growth potential of Polyalphaolefin (PAO) market in terms of value and volume.

2. Capacity By Company

On our online platform, you can stay up to date with essential manufacturers and their current and future operation capacity on a practically real-time basis for Polyalphaolefin (PAO).

3. Capacity By Location

To better understand the regional supply of Polyalphaolefin (PAO) by analyzing its manufacturers' location-based capacity.

4. Plant Operating Efficiency

To determine what percentage manufacturers are operating their plants or how much capacity is being currently used.

5. Production By Company

Study the historical annual production of Polyalphaolefin (PAO) by the leading players and forecast how it will grow in the coming years.

6. Demand by End- Use

Discover which end-user industry: Automotive Industrial, Electrical, Aerospace, Others (Cosmetic etc.) are creating a market and the forecast for the growth of the Polyalphaolefin (PAO) market.

7. Demand by Region

Analyzing the change in demand of Polyalphaolefin (PAO) in different regions, i.e., North America, Europe, Asia Pacific, Middle East and Africa, and South America, that can direct you in mapping the regional demand.

8. Demand by Sales Channel (Direct and Indirect)

Multiple channels are used to sell Polyalphaolefin (PAO). Our sales channel will help in analyzing whether distributors and dealers or direct sales make up most of the industry's sales.

9. Demand-Supply Gap

Determine the supply-demand gap to gain information about the trade surplus or deficiency of Polyalphaolefin (PAO).

10. Company Share

Figure out what proportion of the market share of Polyalphaolefin (PAO) is currently held by leading players across the globe.

11. Manufacturing Process

Discover insights into the intricate manufacturing process of Polyalphaolefin (PAO).

I am satisfied with overall performance of ChemAnalyst. Weekly updates before the final report were especially helpful and reassuring. Additional requests on the interim and/or final reports were handled in a swift and professional manner

Mr.Shin Dosho

Member - Board of Directors

Osaka Gas Co. Ltd

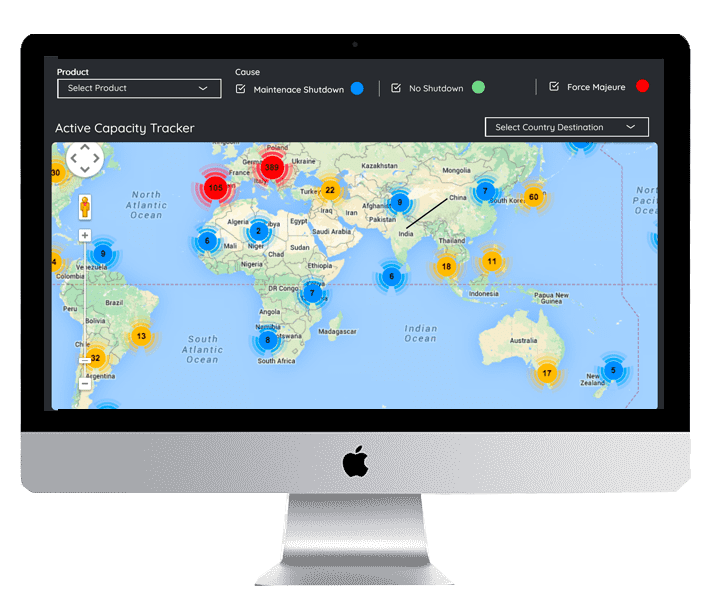

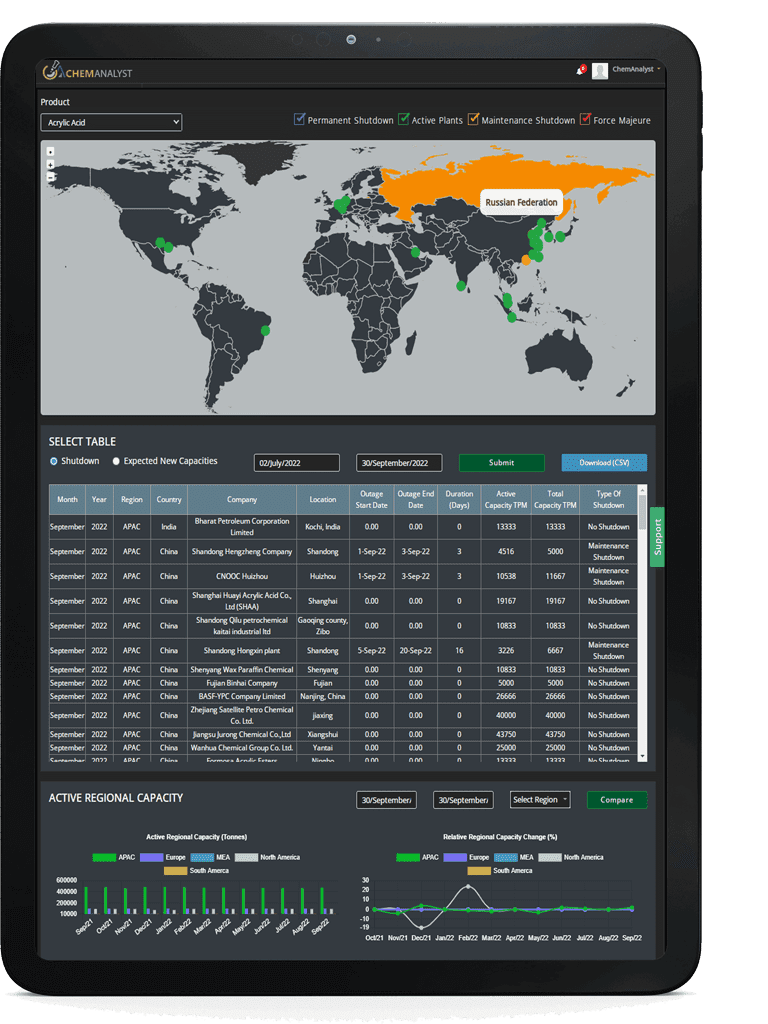

Disruption Tracker

Disruption Tracker reflect the major shutdown on monthly basis which will help you in

tracking the inventory management and smooth functioning of business. Unforeseen shutdowns and disruptions

resulting in a loss of production capacity to impact the bottom line. The capacity tracker provides industries

with a global view of production and consumption capacity loss that reflects the corresponding conversion factors.

It also highlights the immediate impact on supply due to planned and unplanned outages as well as upcoming start-up

of new capacities. Additionally, it emphasizes how each shutdown—whether due to a maintenance turnaround or a case

of force majeure, affects the plant's operating rate for the given duration. Disruption tracker gives a clear insight

into the worldwide outages affecting the commodity of interest. With every shutdown, it also reflects the impact on

supply of the product in the market at a Global level.

The Global Polyalphaolefin (PAO) Market was valued at USD 2625 million in 2025 and is projected to reach USD 4691 million by 2036, growing at a CAGR of 5.43% during the forecast period.

The report covers market sizing and forecasting (2015–2036), segmentation, regional analysis, competitive landscape, and recent strategic developments. It also offers solutions including Custom Research for tailored business strategies.

Our Solutions

Custom Research

We at ChemAnalyst provide tailor-made solutions to our clients based on their requirements which help them in building and expanding their business by developing customized strategy such as sales strategy, GTM Strategy, product portfolio and new product development. Our dedicated team helps clients in getting the best solution for their requirements. We at ChemAnalyst look forward to serving our clients for long term association.

Techno Economic Feasibility Report (TEFR)

ChemAnalyst provide TEFR reports which include market sizing, plant cost (ISBL and OSBL units), financial modelling, covering all the major financial calculations and ratios including production cost, IRR, major technology, licensing fee (if required), and others fixed and variable costs. TEFR reports will help the client to build greenfield project as well as brownfield expansion for a specific geography. Our Team of experts have delivered multiple TEFR reports which help clients in moving ahead of their business competition by grabbing the opportunity and expanding their business portfolio.

Price Benchmarking

Pricing benchmark report provides real-time data perpetuating current market scenarios, in a world that is changing at a rapid pace, having real-time prices is an imperative to make impactful insights and thereby informed decisions. The Price Benchmarking report provides pricing data for an individual market, or group of markets, which can be converted into localized insights and comparable listings. Benchmarking Reports help clients to make informed decisions by construing the data on several filters: region, country, category, grade and subsequently increasing their brand presence. Clients majorly require pricing benchmarks when they opt for a competitive pricing strategy.

We use cookies to deliver the best possible experience on our website. To learn more, visit our

Privacy Policy.

By continuing to use this site or by closing this box, you consent to our use of cookies.

More info.