Global Styrene Copolymer Market Report (2025-2036):

Global Styrene Copolymer Market Size and Growth Forecast

Global Styrene Copolymer Market is projected to grow from USD 6717 million in 2025 to USD 15236 million by 2036, registering a CAGR of 7.79% during the forecast period. As a critical class of engineered thermoplastics, styrene copolymers are synthesized through the bulk, emulsion, or suspension copolymerization of styrene with specialized comonomers such as acrylonitrile, butadiene, or maleic anhydride, mirroring the production of standard general-purpose polystyrene but replacing a portion of the pure styrene monomer with these reactive secondary molecules to structurally eliminate inherent brittleness. This targeted chemical substitution yields substantial competitive advantages over traditional commodity polystyrene equivalents, delivering materials characterized by vastly superior impact toughness, elevated thermal resistance, enhanced chemical barrier properties, and processing benefits like excellent dimensional stability and high-flow moldability. The expanding application scope of these resilient materials is fundamentally supported by strong macroeconomic drivers, particularly the rapid industrial expansion, urbanization, and booming consumer electronics manufacturing sector throughout the Asia-Pacific region. Additionally, stringent regulatory frameworks and emission standards in North American and European markets are actively forcing automotive manufacturers to prioritize component lightweighting initiatives, establishing robust regional economic incentives that continue to accelerate the adoption of these high-performance, versatile polymers as efficient metal substitutes across global industrial supply chains.

Styrene Copolymer Applications in Packaging and Construction Industries

The dominant end-use industries for styrene copolymers encompass automotive manufacturing and advanced packaging solutions, where the material is overwhelmingly selected for its exceptional dimensional stability, superior impact resistance, and high optical clarity. In automotive interior and exterior components, these copolymers provide crucial lightweighting capabilities without sacrificing structural integrity, while in consumer packaging, their excellent moisture barrier properties and thermoforming efficiency make them indispensable for protecting delicate goods. The demand for these advanced polymers is fundamentally propelled by technical superiority requirements across manufacturing sectors, particularly the industrial push for materials that offer high melt flowability and heat resistance to accelerate injection molding cycles and reduce overall manufacturing energy consumption. Concurrently, shifting consumer preferences toward sustainability are driving robust demand for highly recyclable styrenic grades and energy-efficient polymer architectures, which substantially improve the material's environmental footprint while retaining premium mechanical performance. Driven by this confluence of manufacturing performance optimization and sustainable engineering priorities, the styrene copolymer sector is experiencing robust expansion, characterized by increasing market penetration in high-performance consumer durables and expanding adoption across next-generation lightweight industrial applications.

Global Styrene Copolymer Market Segmentation by Resin Type and End-Use Application

The global styrene copolymer market is primarily segmented by product type into Acrylonitrile Butadiene Styrene (ABS), Styrene Acrylonitrile (SAN), Styrenic Block Copolymers (SBCs), and Styrene-Methyl-Methacrylate (SMMA), alongside a secondary segmentation by end-use industry encompassing automotive, consumer electronics, packaging, building and construction, and healthcare. Within this landscape, Acrylonitrile Butadiene Styrene (ABS) currently commands the dominant share of the market, maintaining a leading position due to its exceptional dimensional stability, superior impact resistance, and fundamental cost-effectiveness, all of which have cemented its widespread industrial adoption for manufacturing durable consumer appliances, electronic housings, and lightweight structural automotive components. Conversely, Styrenic Block Copolymers (SBCs)—particularly hydrogenated thermoplastic elastomers like Styrene-Ethylene-Butylene-Styrene (SEBS)—represent the fastest-growing segment with the highest future growth potential. This rapid market expansion is heavily fueled by a surging demand in the advanced healthcare and specialty packaging sectors for specific end-products such as flexible intravenous tubing, pediatric syringe plungers, resilient agricultural films, and flexible housings for wearable medical sensors. The robust acceleration of this emerging segment is primarily underpinned by the unique technical drivers of SBCs, notably their rubber-like elasticity at ambient temperatures, excellent biocompatibility, reliable thermal sterilization stability, and their critical ability to serve as a high-performance, phthalate-free alternative to traditional polyvinyl chloride (PVC) in heavily regulated applications.

Asia-Pacific's Dominant Role in the Global Styrene Copolymer Market

The Asia-Pacific region currently holds the undisputed leading position in the global styrene copolymer market, dominating the international landscape through unparalleled manufacturing scale and intensive infrastructural expansion. This commanding geographical presence is propelled by a robust confluence of aggressive government frameworks, notably including the "Make in India" initiative and East Asian state subsidies that mandate localized advanced material production and stringently regulate energy efficiency in domestic manufacturing. Furthermore, this leadership is intrinsically sustained by a profound shift in regional market sentiment, characterized by rapid urbanization, soaring disposable incomes accelerating domestic consumption, and an escalating societal demand for highly durable, sustainable material solutions. To capitalize on these favorable economic dynamics, the region exhibits a profound commitment to massive capital investment and rigorous research and development, channeling extensive funding into optimizing production efficiencies and synthesizing next-generation, high-performance elastomer grades. Consequently, this intense regional focus on innovation is directly driving the material's diversification, effectively pushing styrene copolymer utility far beyond standard commodity applications and rapidly expanding its integration into cutting-edge sectors, such as electric vehicle lightweighting and advanced medical device manufacturing, thereby solidifying the territory's role as the primary engine for the ongoing global evolution of this chemical category.

Recent Developments and Strategic Initiatives (2025)

The global styrene copolymer market experienced focused strategic advancements between late 2024 and early 2026, characterized by targeted capacity expansions and vital regulatory milestones. Demonstrating a shift toward sustainable manufacturing, Kraton Corporation and Formosa Petrochemical Corporation successfully obtained ISCC PLUS certification in February 2025 for their hydrogenated styrenic block copolymer facility in Mailiao, Taiwan. Production scale also witnessed direct investments to support resilient downstream demand in adhesives and polymer modification, highlighted by Kraton Corporation advancing the mechanical completion of a 24 kiloton per year capacity expansion for styrene-butadiene-styrene copolymers at its Belpre, Ohio plant in 2025. Furthermore, regional supply networks were fortified in Asia as Sinopec Hunan Petrochemical executed extensive project implementations throughout 2025 to optimize and scale its domestic styrenic block copolymer operations. These specific corporate developments underscore a robust sector driven by continuous facility enhancements and process innovation tailored to meet evolving end-user requirements.

Key Players in the Global Styrene Copolymer Market

Major players in the Global Styrene Copolymer market are Baling Petrochemical and Hainan Refining & Chemical JV, China Petroleum Corporation, Kraton Performance Polymers, Inc., TSRC corporation, Others

Years considered for this report:

Historical Period: 2015-2024

Base Year: 2025

Estimated Year: 2026

Forecast Period: 2026-2036

This report will be delivered through an online digital platform with a one-year subscription, along with quarterly updates.

Objective of the Study:

• To assess the demand-supply scenario of the Styrene Copolymer, covering production, demand, and supply at the global level.

• To analyze and forecast the market size of Styrene Copolymer

• To classify and forecast the Global Styrene Copolymer market based on end-use industries and regional distribution.

• To examine competitive developments in the global Styrene Copolymer market, such as expansions, mergers & acquisitions, and other strategic initiatives.

Research Methodology: How Was the Styrene Copolymer Market Data Collected?

To extract data for the Global Styrene Copolymer market, primary research surveys were conducted with Styrene Copolymer manufacturers, suppliers, distributors, wholesalers, and traders. During the interviews, respondents were also asked about their competitors.Through this approach, ChemAnalyst was able to identify and include manufacturers that could not be captured through secondary research due to its limitations.Moreover, ChemAnalyst analyzed various market segments and projected a positive outlook for the Global Styrene Copolymer market over the coming years.

ChemAnalyst calculated the global demand for Styrene Copolymer by analyzing the volume consumed by end-user industries. The forecast was developed based on the growth rates of these end-use industries. These values were obtained from industry experts and company representatives and were externally validated by analyzing the historical sales data of respective manufacturers to determine the overall market size. Additionally, various secondary sources, such as company websites, association reports, and annual reports, were reviewed by ChemAnalyst.

Key Target Audience for This Report

• Styrene Copolymer manufacturers and other industry stakeholders

• Organizations, forums, and alliances related to Styrene Copolymer distribution

• Government bodies, including regulatory authorities and policymakers

• Market research organizations and consulting firms

The study provides insights into several critical ques tions relevant to industry stakeholders, including Styrene Copolymer manufacturers, customers, and policymakers. It also helps identify high-growth segments over the coming years, thereby supporting stakeholders in making informed investment decisions and facilitating strategic expansion.

Report Scope and Market Segmentation Framework

In this report, the Global Styrene Copolymer market has been segmented into the following categories. In addition, key industry trends have been detailed below:

Attribute

Details

Market size Value in 2025

USD 6717 Million

Market size Value in 2036

USD 15236 Million

Growth Rate

CAGR of 7.79% from 2026 to 2036

Base year

2025

Estimated year

2026

Historical Data

2015 - 2024

Forecast period

2027 - 2036

Quantitative units

Demand in thousand tonnes and CAGR from 2026 to 2036

Report coverage

Industry Market Size, Capacity By Company, Capacity by Location, Operating Efficiency, Production by Company, Demand by End- Use, Demand by Region, Demand by Sales Channel, Demand-Supply Gap, Company Share, Manufacturing Process, Policy and Regulatory Landscape.

Segments covered

By End-Use: (Shoe Material, Modification Asphault, Polymer Modification, Adhesives, and Waterproofing Membrane) By Sales Channel: (Direct Sale and Indirect Sale)

Regional scope

North America, Europe, Asia Pacific, Middle East and Africa, and South America.

Market Data & Insights

Table of Content

1. Industry Market Size

It is an essential metric for market analysis, as it provides insights into the overall size and growth potential of Styrene Copolymer market in terms of value and volume.

2. Capacity By Company

On our online platform, you can stay up to date with essential manufacturers and their current and future operation capacity on a practically real-time basis for Styrene Copolymer.

3. Capacity By Location

To better understand the regional supply of Styrene Copolymer by analyzing its manufacturers' location-based capacity.

4. Plant Operating Efficiency

To determine what percentage manufacturers are operating their plants or how much capacity is being currently used.

5. Production By Company [Quarterly Update]

Study the historical annual production of Styrene Copolymer by the leading players and forecast how it will grow in the coming years.

6. Demand by End- Use [Quarterly Update]

Discover which end-user industry (Shoe Material, Modification Asphault, Polymer Modification, Adhesives, and Waterproofing Membrane) are creating a market and the forecast for the growth of the Styrene Copolymer market.

7. Demand by Region

Analyzing the change in demand of Styrene Copolymer in different regions, i.e., North America, Europe, Asia Pacific, Middle East and Africa, and South America, that can direct you in mapping the regional demand.

8. Demand by Sales Channel (Direct and Indirect)

Multiple channels are used to sell Styrene Copolymer. Our sales channel will help in analyzing whether distributors and dealers or direct sales make up most of the industry's sales.

9. Demand-Supply Gap

Determine the supply-demand gap to gain information about the trade surplus or deficiency of Styrene Copolymer.

10. Company Share

Figure out what proportion of the market share of Styrene Copolymer is currently held by leading players across the globe.

11. Manufacturing Process

Discover insights into the intricate manufacturing process of Styrene Copolymer.

12. Policy and Regulatory Landscape

Gain a comprehensive understanding of the policy and regulatory landscape within the Styrene Copolymer market.

I am satisfied with overall performance of ChemAnalyst. Weekly updates before the final report were especially helpful and reassuring. Additional requests on the interim and/or final reports were handled in a swift and professional manner

Mr.Shin Dosho

Member - Board of Directors

Osaka Gas Co. Ltd

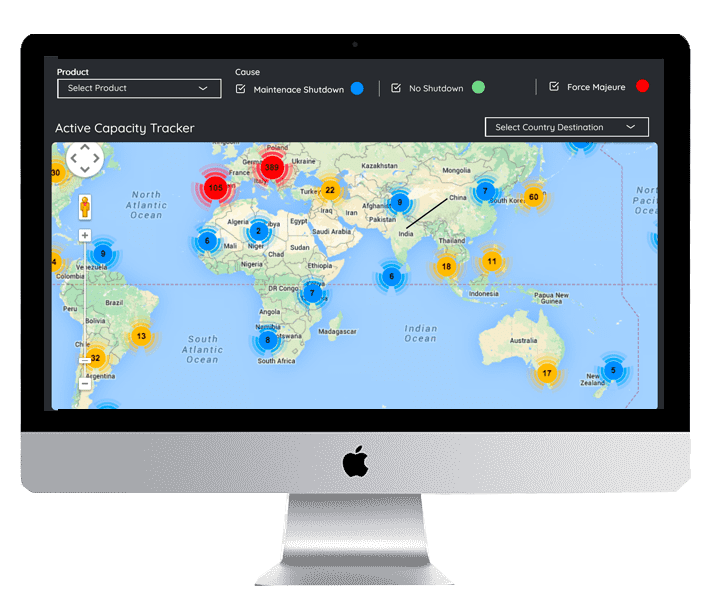

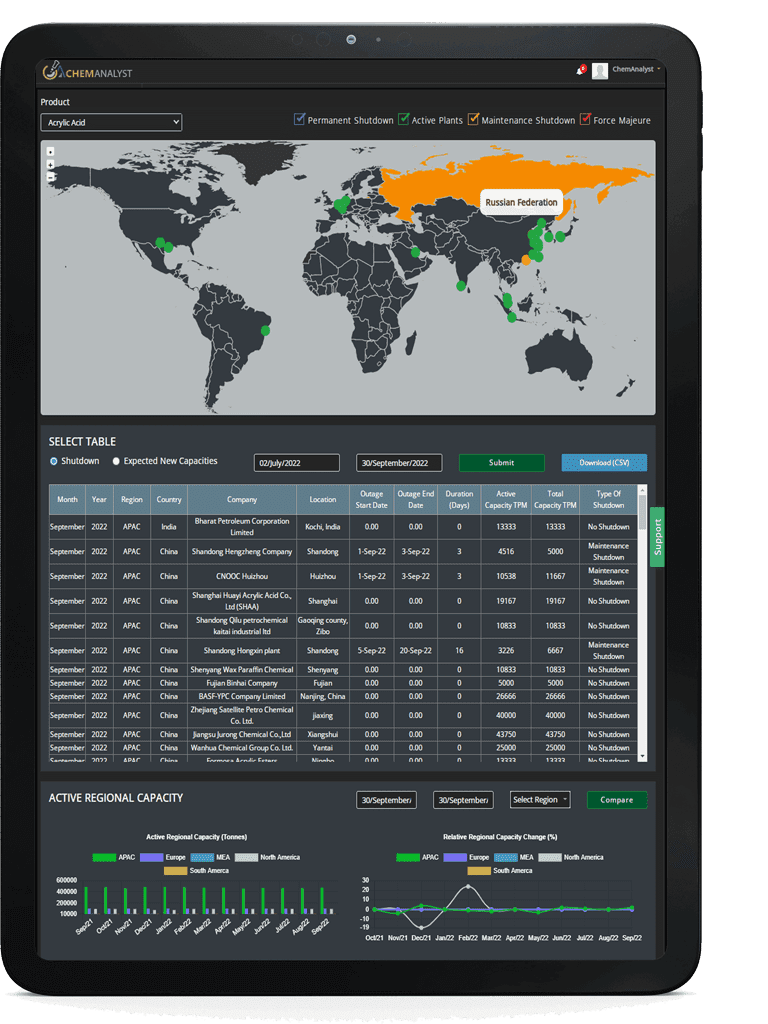

Disruption Tracker

Disruption Tracker reflect the major shutdown on monthly basis which will help you in

tracking the inventory management and smooth functioning of business. Unforeseen shutdowns and disruptions

resulting in a loss of production capacity to impact the bottom line. The capacity tracker provides industries

with a global view of production and consumption capacity loss that reflects the corresponding conversion factors.

It also highlights the immediate impact on supply due to planned and unplanned outages as well as upcoming start-up

of new capacities. Additionally, it emphasizes how each shutdown—whether due to a maintenance turnaround or a case

of force majeure, affects the plant's operating rate for the given duration. Disruption tracker gives a clear insight

into the worldwide outages affecting the commodity of interest. With every shutdown, it also reflects the impact on

supply of the product in the market at a Global level.

The Global Styrene Copolymer Market was valued at USD 6717 million in 2025 and is projected to reach USD 15236 million by 2036, growing at a CAGR of 7.79% during the forecast period.

Styrene Copolymer is used in a wide range of end use industries including Shoe Material, Modification Asphault, Polymer Modification, Adhesives, and Waterproofing Membrane.

Major players include Baling Petrochemical and Hainan Refining & Chemical JV, China Petroleum Corporation, Kraton Performance Polymers, Inc., TSRC corporation, Others.

The report covers market sizing and forecasting (2015–2036), segmentation, regional analysis, competitive landscape, and recent strategic developments. It also offers solutions including Custom Research for tailored business strategies.

Our Solutions

Custom Research

We at ChemAnalyst provide tailor-made solutions to our clients based on their requirements which help them in building and expanding their business by developing customized strategy such as sales strategy, GTM Strategy, product portfolio and new product development. Our dedicated team helps clients in getting the best solution for their requirements. We at ChemAnalyst look forward to serving our clients for long term association.

Techno Economic Feasibility Report (TEFR)

ChemAnalyst provide TEFR reports which include market sizing, plant cost (ISBL and OSBL units), financial modelling, covering all the major financial calculations and ratios including production cost, IRR, major technology, licensing fee (if required), and others fixed and variable costs. TEFR reports will help the client to build greenfield project as well as brownfield expansion for a specific geography. Our Team of experts have delivered multiple TEFR reports which help clients in moving ahead of their business competition by grabbing the opportunity and expanding their business portfolio.

Price Benchmarking

Pricing benchmark report provides real-time data perpetuating current market scenarios, in a world that is changing at a rapid pace, having real-time prices is an imperative to make impactful insights and thereby informed decisions. The Price Benchmarking report provides pricing data for an individual market, or group of markets, which can be converted into localized insights and comparable listings. Benchmarking Reports help clients to make informed decisions by construing the data on several filters: region, country, category, grade and subsequently increasing their brand presence. Clients majorly require pricing benchmarks when they opt for a competitive pricing strategy.

We use cookies to deliver the best possible experience on our website. To learn more, visit our

Privacy Policy.

By continuing to use this site or by closing this box, you consent to our use of cookies.

More info.